Editor's note: Seeking Alpha is proud to welcome Jagnoor Singh Virk as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

puhimec/iStock via Getty Images

Investment thesis

Supremex (TSX:SXP:CA) (OTCPK:SUMXF), the second largest manufacturer of envelops in North America with a burgeoning packaging segment, presents a compelling value story that is backed by solid fundamentals and a coherent corporate strategy. In my view, the firm's substantial free cash flow generation, growth opportunity in packaging and a solid M&A track record, makes it a compelling Buy, particularly in light of its modest FY23E EV/EBITDA multiple of 4x. I believe the company's growing footprint in the packaging segment has been largely overlooked by investors who have been too focused on the envelop business, which has been coping with declining volumes. Though, SXP has, to a large extent, counteracted the envelop industry's secular declines by wielding its 90% Canadian market share to protect rates while also growing its US footprint to offset volume losses. On the packaging front, the company has built out a robust product suite through acquisitions, which I expect will benefit from the long-term growth of the industry.

Envelop: Combatting the industry headwinds

Supremex began in 1977 as an independent envelope provider, eventually pursuing a string of acquisitions to become the largest purveyor of envelopes in the country. Given that nearly all Canadian letter mail is transactional, the industry has seen a 5-6% decline in volumes per year, which reflects the shift of financial institutions towards digital billing. In the US, the envelope market is much more fragmented with Supremex owning a ~7% market share, making it a top five operator in the country. While the US market is competitive, it is also largely localized (based on delivery radius) and contains several small private players that can either be acquired or outcompeted by Supremex, particularly in the north-eastern US where it currently operates. Despite softening industry trends, Supremex has managed to deliver ~7% CAGR revenue growth over the prior five years. In my view, Supremex's multi-pronged approach to revenue growth, which includes price action & acquisitive growth, can be sustained over the medium to long term.

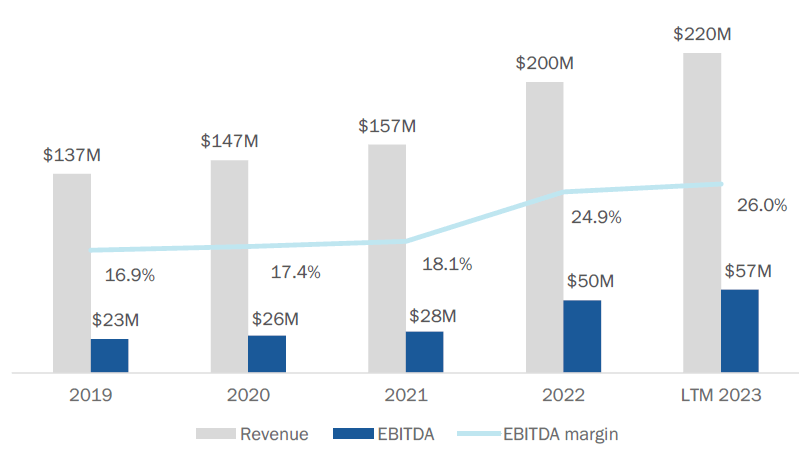

Figure 1: Envelop Segment Revenue and EBITDA (FY19 - LTM FY23)

Supremex Company Reports

A key consolidator in the envelop market

The key for Supremex in the Canadian space has been generating scale and pricing power. By acquiring several of its main competitors, the firm has essentially monopolized the industry, with only small independent shops competing for its clients. Given the importance of reliability when mailing customer data and demand for aesthetic customization, large Canadian corporations are generally looking for a sizeable partner that has the flexibility to adhere to their needs. In tandem with the relatively low cost of envelopes, Supremex's market position provides a degree of pricing power on its customers. Importantly, the market faces minimal competition from international operators as the cost of shipping bulk envelopes is often prohibitively expensive.

Figure 2: SXP Canadian roll-up story

Supremex Company Reports

Spreading tentacles in US through share gain and strategic acquisitions

As a method of geographical diversification, Supremex expanded its operations into the northern United States with its 2015 acquisition of Classic Envelope Inc. Classic gave SXP a well-known US brand and customer list, allowing it to poach US customers and take market share from smaller private operators. As of 2022, the US business represent 45% of the envelope segment, attained through a combination of acquisitions and organic growth. Looking forward, I expect the US business to see organic volume growth driven by continued share gains in the much larger US market (~US$2 billion in sales).

Packaging: A segment that adds growth angle to SXP story

Supremex's packaging business primarily focuses on folding carton, ecommerce products, and specialty offerings. The paper packaging industry continues to experience secular growth, with folding carton industry expected to grow at a CAGR of 5-5.25%, over the next five years. I believe, this is largely expected to continue, driven by the continued shift away from plastic packaging, the increasing number of consumer products being offered, and the further adoption of ecommerce, particularly in North America.

Figure 3: Packaging Revenue and EBITDA (FY19 - LTM FY23)

Supremex Company Reports

Active on the M&A front

SXP has made six packaging acquisitions over the past seven years, deploying $69M in capital over that period. Management has been prudent in its inorganic growth strategy, finding highly synergistic businesses that (1) increase the breadth of its production capabilities focused on niches, (2) create opportunities to improve scale and factory utilization, and (3) give it access to geographies it had not previously served. The company's recent acquisition of Paragraph effectively illustrates the firm's strategy. The transaction gives SXP scale in Quebec, adding two facilities in the province and solidifying the company's premier position in Quebec's folding carton market. Furthermore, Paragraph adds to SXP's capabilities in digital and wide format printing, which are services it can cross-sell to customers across its entire footprint. Once acquired, Supremex works to optimize its footprint, shifting equipment and employees between facilities which creates significant synergies, maximizing the revenue opportunity while eliminating cost redundancies.

Targeting 50% packaging contribution by FY25

Management has stated its objective of reaching $200M+ in segment revenue by 2025, which would allow the company to generate roughly half of its consolidated sales from the growthier packaging business. Given that the segment delivered LTM revenue of ~$77M, the company will need to use an assortment of growth prongs to deliver its goal - leaning on US packaging acquisitions to secure contract wins, product suite expansion, and the overarching growth of the folding carton industry. The target of more than doubling the revenue from a business segment over the course of a couple years might come across as over-ambitious, but taking into account the company's solid M&A execution in US, along with the backdrop of a secular growth trend in the folding carton industry, I believe the target is achievable.

Seasoned CEO at the helm

Steward Emerson has been with the company for more than 30 years and was appointed President and CEO of Supremex in September 2014. Under his leadership, Supremex has successfully rolled up the Canadian envelope market, expanded into the US and diversified into the growing packaging industry. Given his robust industry relationships and proven expertise, I am confident that Mr. Emerson possesses the requisite leadership qualities to guide Supremex towards realizing its long-term growth strategy.

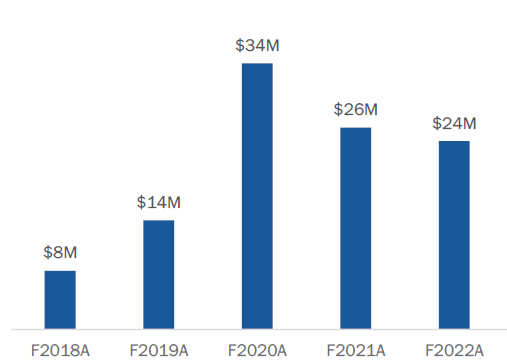

Ample FCF generation gives firepower to pursue inorganic growth while maintaining current dividend payout

A key tenet of the SXP thesis is the firm's ability to generation substantial FCF, allowing it to moderate leverage and support its acquisition-based growth strategy. The firm has espoused an "acquire, integrate, de-lever" mandate, which focuses on managing its debt load to finance transactions. The crux of Supremex's strategy relies on the cash flow generative nature of its businesses, with both segments generating mid-teen margins and requiring minimal capital. Over the last five years, Supremex has generated $106M in cumulative free cash flow, which has allowed it to keep net debt/EBITDA below 1.3x despite several large-scale acquisitions. Apart from leveraging the fattish cash flow to pursue acquisitive growth, the company has also returned capital to shareholders via dividends and share buybacks. The current quarterly dividend stands at 0.035/share, which translates into a dividend yield of 3.2%. In my view, considering the moderate debt level & management's focus on pursuing smaller tuck-in acquisitions going forward, the current dividend is likely to be sustainable for the foreseeable future. On the buyback front, the company repurchased 131,700 share (or 10% of allowable limit) for ~$650K under the NCIB that ran through August 31, 2022 to August 18, 2023. As of August 29 2023, the company has renewed its NCIB, and in my view, the buybacks will stay in place for FY23 & FY24, providing further support for high single digit y/y EPS growth.

Figure 4: SXP FCF (FY18 - FY22)

Supremex Company Reports

Valuation: Attractive with re-rating potential on shift towards packaging

SXP trades at a reasonable 4x EV/F23E EBITDA against consensus estimates per Capital IQ, which commensurate with an envelope manufacturer in a cyclically declining industry. In my view, the packaging aspects of the business are largely being overlooked by investors, which has created an attractive BUY opportunity. Longer term, I expect that the firm's shift towards packaging will result in multiple expansion, putting it more in line with packaging comparables that trade at a mean ~7.8x EV/FY24 EBITDA multiple (Figure 6).

My target price for Supremex is $8.40, which is based on sum-of-the-parts valuation methodology. Please see below for my assumptions:

- The sums-of-the-parts valuation methodology is warranted because both business segments, namely Envelop and Packaging, are very different in terms of growth prospects and each deserves a valuation multiple which clearly reflects that variation. While Envelop business is in structural decline, the packaging segment has very favorable growth outlook.

- I'm applying a 4x EV/EBITDA multiple to the FY24 EBITDA estimates for the Envelop segment. I assume that the company will generate 60%of EBITDA from the Envelop segment by FY24, which translates into EBITDA of $35M, when calculated as $59M*60%, where $59M is the consensus FY24 EBITDA for the entire company as per Capital IQ. Lastly, the 4x EV/EBITDA multiple reflects no expansion/contraction from where the stock currently trades, which flows from my opinion that for foreseeable period, Supremex will be able to sustain revenues at the current level in the envelop segment through price action and acquisitive growth.

- I'm applying a 5.8x EV/EBITDA multiple to the FY24 EBITDA estimates for the Packaging segment. I assume that the company will generate 40.0%of EBITDA from the Packaging segment by FY24, which translates into EBITDA of $24M, calculated as $59M*40.0%, where $59M is the consensus EBITDA for entire company as per Capital IQ. Additionally, the 5.8x EV/EBITDA multiple presents a ~2x discount to peers (Figure 6), which compensates for SXP's relatively smaller size and lower liquidity.

Based on market close price of $4.39 as of 10th September, my target price of $8.40 for SXP presents an upside of 91.3%.

Figure:5 Valuation Table ($CAD)

|

FY24 Envelop EBITDA |

$35M |

|

Target EV/EBITDA Multiple for Envelop segment |

4.0x |

| (A) Envelop segment valuation |

$140M |

|

FY24 Packaging EBITDA |

$24M |

|

Target EV/EBITDA Multiple for Packaging segment |

5.8x |

|

(B) Packaging segment valuation |

$139M |

|

Sum Of The Parts Enterprise Valuation (A) + (B) |

$279M |

|

Less: FY24 Consensus Net Debt |

$61M |

|

FY24 Equity Value |

$218M |

|

Outstanding Shares |

|

|

Target Price |

$8.40 |

Source: Capital IQ, Author's estimates

Figure:6 Comparable Companies ($CAD)

|

Packaging Company |

Price |

Market Cap ($M) |

F24E EV/EBITDA |

|

Berry Global Group Inc |

$85.3 |

$10,074.4 |

|

|

CCL Industry Inc. Class B |

$58.44 |

$10,401.0 |

|

|

Graphic Packaging Holding Company |

$29.8 |

$9,167.7 |

|

|

Grief Inc Class A |

$93.2 |

$4,419.4 |

|

|

International Paper Company |

$47.1 |

$16,308.6 |

|

|

Packaging Corporation of America |

$198.9 |

$17,757.1 |

|

|

Silgan Holdings Inc. |

$58.1 |

$6,390.1 |

|

|

Sonoco Products Company |

$74.24 |

$7,274.7 |

|

|

WestRock Company |

$46.5 |

$11,886.3 |

|

|

Average |

7.8x |

Source: Capital IQ, prices as of September 10, 2023

Key risks to target price

More rapid declines in Canadian envelope usage would present downside to estimates: The Canadian envelope market has experienced mid-single-digit annual volume declines over the previous five years as transactional communications become increasingly digital. If the push towards paperless billing accelerates, it would likely cause a more rapid revenue decline.

US operations may be unable to gain meaningful market share: Management expects the expansion of its US business will help offset reductions in Canadian volumes, with ultimately US market share effectively offsetting the entirety of Canadian declines. While the US market is more resilient with a focus on direct mail, the market is highly competitive, which could prevent meaningful share gains.

Packaging growth may slow in an economic downturn: The packaging segment has been a growth driver for SXP with a focus on developing custom solutions for consumer-facing businesses. If non-discretionary spending declines, SXP's customers may see declines in required volumes. Our current forecasts include low single-digit organic growth in packaging.

SXP may not be able to acquire and integrate assets effectively. There is a risk that the company fails to find attractive, well-priced assets for acquisition, or that the assets it does acquire are unable to be integrated into the broader ecosystem. While the company boasts an impressive track record, all acquisitions come with risks of customer loss, key employee and service provider loss, and greater-than-expected costs.

Conclusion

Supremex appears to have largely been overlooked by investors, but based on the points discussed above and the results of my sum-of-the-parts valuation analysis, I rate Supremex a Strong Buy.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

"story" - Google News

September 14, 2023 at 12:38AM

https://ift.tt/7hvzu1j

Supremex Stock: A Value Story Hidden Inside The Envelop (OTCMKTS:SUMXF) - Seeking Alpha

"story" - Google News

https://ift.tt/nsduqRj

https://ift.tt/x2S13C4

Bagikan Berita Ini

0 Response to "Supremex Stock: A Value Story Hidden Inside The Envelop (OTCMKTS:SUMXF) - Seeking Alpha"

Post a Comment